Redraw versus Offset.What’s the Difference?

Activating a redraw feature or adding an offset account to your home loan can help you cut down on interest payments. Let’s explore how they work differently and figure out which one suits you best.

Here's what we'll cover:

-

Understanding how to manage your debt

- Explaining what offset and redraw are

- Highlighting the main differences between them

- How they can help reduce your home loan interest

- Deciding which one might be better for you

- Clarifying how redraw is different from a line of credit

How Offset and Redraw Work?

Offset accounts and redraw features are similar in that they both let you use extra money to lower your loan interest. But there are some key distinctions you should know before choosing one.

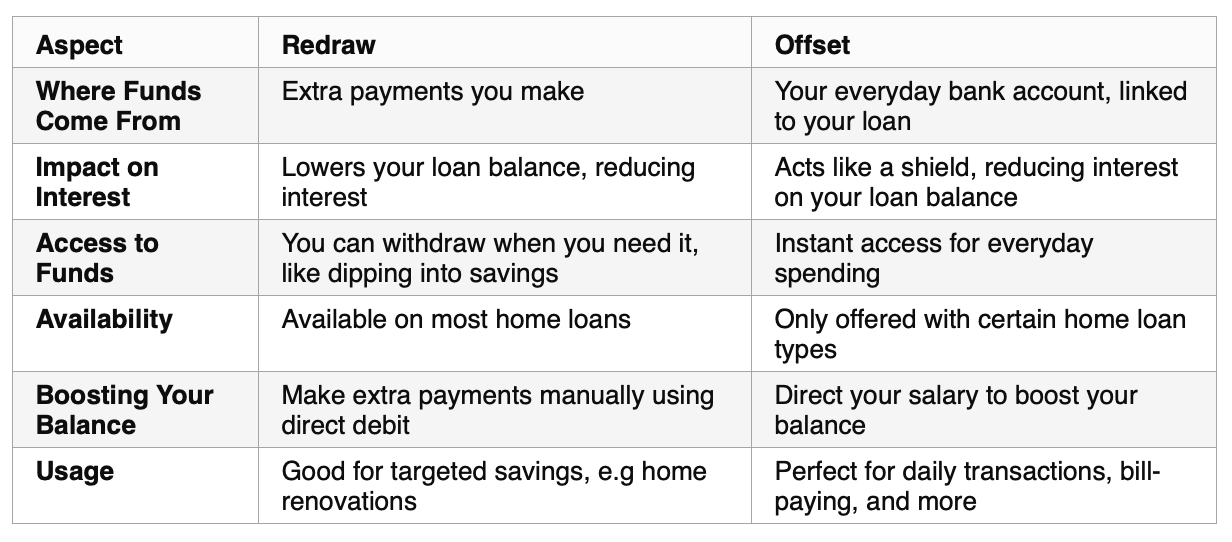

Redraw

Think of a redraw as your loan’s secret stash. With redraw, you can put in extra money on top of your regular repayments. If you need that cash for something like renovations or an unexpected expense, you can take it out again.

The money you put into your redraw lowers your loan balance, which means you pay less interest. Just keep in mind that as you make your regular payments, that extra cash you put in gradually decreases over time.

Offset

An offset account is like having a separate savings account linked to your loan. It works just like a regular bank account, so you can deposit and withdraw money whenever you need to. But here’s the cool part: the more money you keep in your offset account, the less interest you pay on your loan.

The funds in your offset account offset against your loan balance, which reduces the interest you owe. But remember, as your account balance goes up and down, so does the amount of interest you save.

Spotting the Differences

The big difference is how they handle your money. With redraw, your extra payments go into your loan balance. But with offset, your money sits in a separate account, doing its thing.

Reducing Home Loan Interest

Both offset accounts and redraw features work the same way to lower your loan interest. By making extra payments or keeping extra funds in an offset account, you chip away at your loan balance, which means less interest to pay.

Choosing Between Redraw and Offset

The big question: which one is better for you? It depends on how you handle your money. If you regularly make extra payments or want to have a stash you can dip into, redraw might be the way to go. But if you prefer easy access to your money and want everything in one account, offset could be your best bet.

Oh, and don’t forget about taxes – they can make a difference too. If you plan to rent out your home and have it as an investment property and buy a new home there might be different tax implications for offset and redraw. That because if you have money in an offset account on your original home, you can then use this money to buy your new home. This means you get to maintain the deductibility of intrest on your rented home Alternatively, If you used a redraw, the intrest would NOT be deductible.

Considering the Line of Credit Option

While redraw and offset are often compared, they serve different purposes than a line of credit. Redraw and offset help you manage your loan and save on interest, while a line of credit is more like a flexible loan that lets you borrow money as needed. This is perfect for people who have paid off their home and want to access the equity.

Summing It Up

Both redraw features and offset accounts help you save on your home loan interest. Which one you choose depends on your financial situation and how you like to manage your money.

I hope you enjoyed reading this article. If you would like my team and I to help you structure your loans correctly, please contact us for a free no obligation meeting. - Chris Tolevsky

Arrange Your FREE

No-Obligation Meeting

Please complete the form below

Download now and get your

business off to a flying start!