How To Protect Your Loved Ones From Financial Ruin. The Shocking Truth You Must Discover About Wills...

Do you have a Will?

If so, is your Will set up to protect your assets and minimise tax of your family?

Most Wills do NOT do this and that is why they are known as "standard" Wills.

There is a much better way of setting up your Will which can provide you with significant tax advantages . It can also, protect your your families assets against divorce, creditors and bankruptcy for three generations.

Let me explain...

You see, when it comes to making out a will , generally it is made along the following lines:

"Everything I own is to go to my partner "B" and should they die before me or at the same time as me then everything is to go to

our children "C". The partner then writes a similar will in favour of the first person "A"

Now consider the following scenario. "A" dies and leaves everything to "B". "B" remarries "X" – "X" has their own children. When "B" dies everything they own then goes to "X". Upon "Xs" death everything goes to either THEIR children not to "C"! "C" may contest the will however it has been clearly demonstrated in court that "C" has little change of winning!

One way of alleviating the "remarrying" problem is to have both parents make a "deed of mutual wills as a contract". In this case both parents enter into a legal contract with each other that basically says "I'll give it all to you "B" on the condition that when you pass away everything goes to "C". This gives the right for everything to to end up in "Cs" hands. Even if "B" marries "X", all the assets passed on at "As" death have to go to "C". "X" and their children cannot get any of these assets!

The above example is what is known as a "Standard Will" and is not tax effective and provides no asset protection. This is because the assets are passed on to an individual which means they are soley responsible for the tax on income received. Also, if the person receiving the inheritance goes bankrupt or gets divorced, the assets can be taken from them.

What are our clients major concerns?

- They want to protect their children’s future inheritance against the potential of divorce and keep their inheritance within the family bloodline. i.e. Grandchildren.

- They are concerned that their children’s business or profession could put them at risk of being sued and losing their inheritance if they were to become bankrupt.

- The want to avoid death taxes on superannuation when paid to non-dependant children at 17% and 32% on the taxable component.

- They want to minimise their tax by having flexibility with the way they distribute income.

- They want to protect vulnerable children and those with special needs.

The Solution

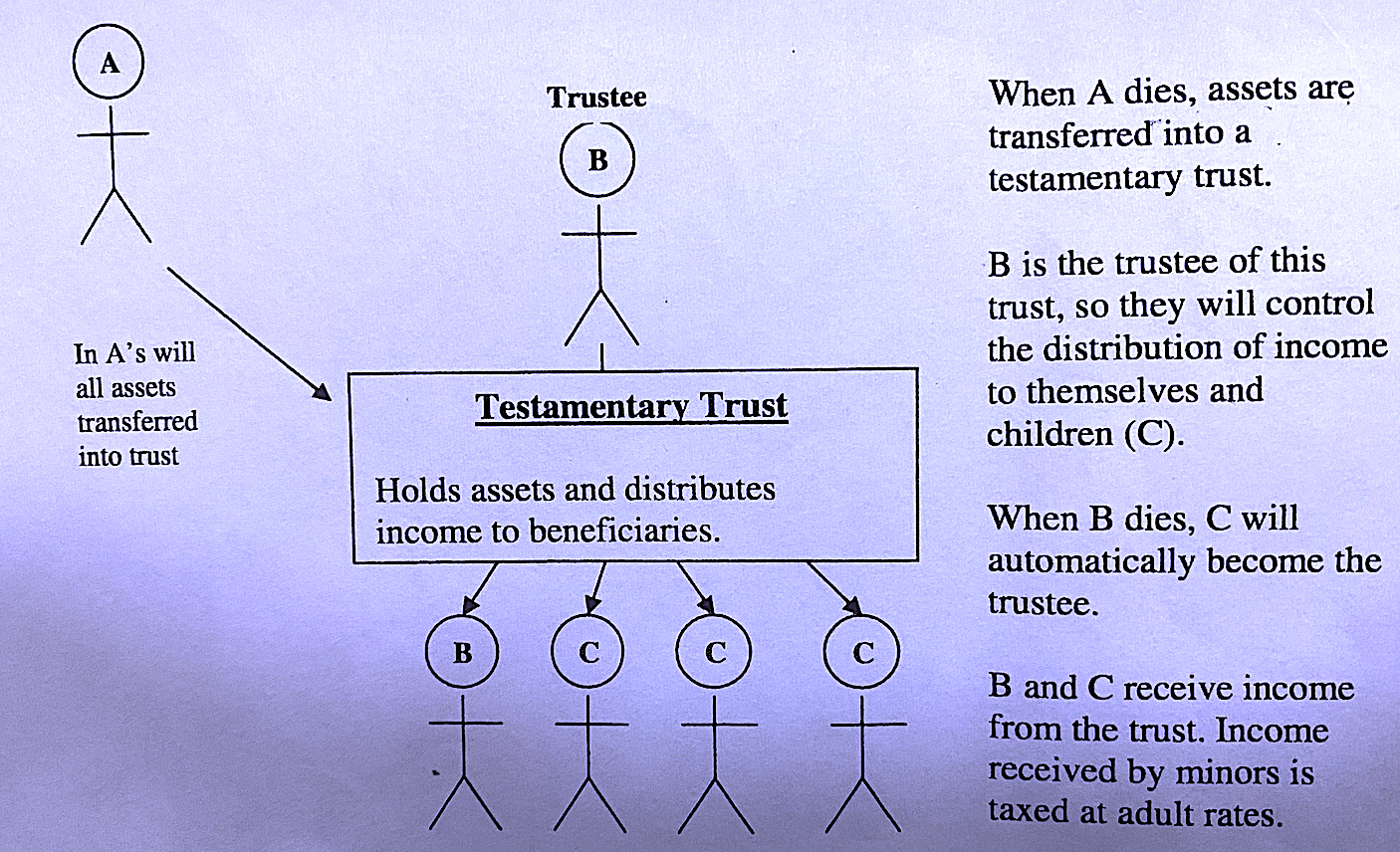

Another popular, but little known strategy is for the deceased to leave their assets in a "testamentary trust" upon their death. In this case "A" leaves the assets in the testamentary trust with "B" and "C" as the beneficiaries. "B" is nominated as the trustee of the trust and upon their death it is predetermined that "C" becomes the trustee (i.e."C" then controls the assets). So then "B" and then "C" have the control of the trust.

It looks like this;

The advantages of this structure

- Minors (ie children under 18 years of age) are taxed as adults. In normal tax law when a child is under 18 and receives a "passive income" from a trust, dividends, rent, interest or the like, they are allowed to earn the first $416 per annum tax free and then any amount over this is taxed at 60%. However under a testamentary trust, they are taxed at normal adult rates. ie the first $20,542 tax free and the remainder at normal adult tax rates. This is a major tax planning strategy for those with young children.

- The protection of pensions for (non spouse) beneficiaries.

- Entitlement to income can be varied each year at the discretion of the trustee (in this case "B").

- Capital gains tax exemptions on the death of "A".

- The protection of the beneficiaries against creditors and bankruptcy

- The protection of the beneficiaries inheritance against divorce

- The control of assets against spendthrift beneficiaries

- The protection of vulnerable beneficiaries and those with special needs

- The tax on super to non-dependants has the potential to be reduced from 17% and 32 % to nil.

Case study

Tom and Nicole own real estate valued at 1.5 million, shares of

The clients biggest concerns

- Daniels marriage may not last and are worried about the effect a divorce would have, after their death, both on their son and the rest of the family, if property needed to be sold to payout Daniel's spouse in a divorce settlement.

- Susan operates a small business and is not very good with managing money . Creditors are continually chasing her for unpaid bills and as a result she is always borrowing more money to keep her business afloat. Tom and Nicole are concerned that any inheritance they leave to Susan in their Wills will go towards paying off creditors of the business.

- Daniel and Susan are full time employees and not tax dependants which means they will have to pay 17% or 32% on any superannuation benefit they receive.

- Tom and Nicole want to pass on control of their Family Trust to their children. They know that Family's Trusts are not covered in Wills and wan't a succession plan.

- Tom and Nicole want their children and grandchildren to receive as much of the income as tax free from the trust to maximise the return on their assets.

Our clients wishes

Tom and Nicole, want to ensure that the assets left to their children are not lost if one or more of them divorce, face creditor demands or bankruptcy. The value of capital assets remains in their family for generations to come. Their children have tax flexibility that will, in effect, allow them to educate Tom and Nicole's grandchildren with pre-tax dollars and to minimise the tax burden by sharing income among a wide range of family members and the tax on superannuation is reduced to zero.

Tolevsky Partners recommendations

- Prepare new for Tom and Nicole in place of standard Wills, by setting up Mutual 3 -Generation Testamentary Trust Wills

- The Trust’s would begin on the death of the first of Tom or Nicole and operate for up to 80 years. The survivor of Tom and Nicole would retain full control of the trusts until the survivor's death. At this time the control of each trust would pass to the children.

- The beneficiaries of each Trust will be the surviving spouse, the particular child and their bloodline.

- Under the rules of each Trust, the spouses of children and grandchildren, may, at the trustee’s discretion, receive income, but capital is prevented from passing outside the bloodline.

- Superannuation Binding Death Nominations for Tom and Nicole were updated with the beneficiary as "Legal Personal Representative" so as to allow them the option of all their superannuation proceeds on death being distributed into their 3 -Generation Testamentary Trust.

- A deed of variation of the Family Trust to appoint the children as back up Appointor's. This gives the children the power to appoint themselves as Trustee's and manage the Family Trust and benefit from the investments.

The Result

Daniel's Trust will ensure that if, he were to get a divorce, his inheritance will be protected from ‘attack’ by the Family Court. Susan's Trust will ensure that if her business runs into problems, her share of the estate will be protected from creditors making any claims.

The Super Testamentary Trust's seek to reduce the non-dependant tax tax from 17% and 32% to 0%.

When income from a testamentary trust is distributed to a minor i.e. a child under the age of 18, they will be taxed at adult tax rates. For example, with the low income rebate the first $20,452.00 will be tax-free.

Each Trust will operate to ensure that control of the value of the family assets will remain in the hands of Chris and Pauline’s descendants for as long as they wish and can be wound up at any time, giving the beneficiaries complete flexibility.

Take action NOW before it's too late!

A "Standard Will" does NOT provide protection for assets in the

event of divorce or creditor" attack" for the next generation. It also leaves you open to death tax on your super if your

children are no longer dependants.

the

event of divorce or creditor" attack" for the next generation. It also leaves you open to death tax on your super if your

children are no longer dependants.

This is why leaving assets to beneficiaries in a 3-Generation Testamentary Trust provides complete flexibility which is the most important thing when it comes to Estate Planning.

This is because we don’t know; 1. When we will die, 2. What assets we will have when we die and 3. What the tax laws will be at that time. It ensures the value of assets remain in the family bloodline, plus, as a bonus, significantly improves the taxation position, once Tom or Nicole have died, due to increased income distribution flexibility.

Remember, the worst thing you can do is die "intestate" (i.e. without a will). In this case it is more complicated to administer your Estate and your assets may not be distributed according to your wishes.

Book your complimentary consultation

If you would like to set up a Testamentary Trust or review your situation, we invite you to BOOK

NOW for

a complimentary consultation to discuss your needs. As Estate Planning Specialists we are qualified to develop a

comprehensive Estate Plan for you including setting up your Wills, enduring and medical power of attorney. Our aim is to

give you peace of mind that your estate is protected for future generations.

Arrange Your FREE

No-Obligation Meeting

Please complete the form below

Download now and get your

business off to a flying start!