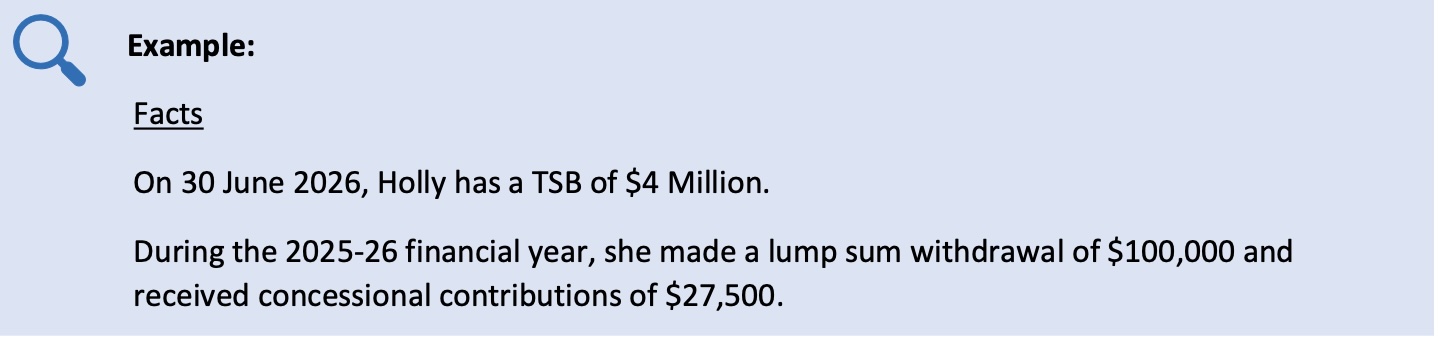

New Super Tax Nightmare

If Freddy Krueger ever swapped his bladed glove for a calculator, Section 296 might be his handywork. This proposed new "super tax" is targeting high superannuation balances with the same stealth and sting as a horror movie villain.

Set to apply from the 2025–26 financial year, the tax aims to dig deeper into the pockets of those whose Total Superannuation Balance (TSB) exceeds $3 million at the end of a financial year.

It doesn’t ask permission. It doesn’t ease in gently. And for many, especially in an economy already rattled by inflation and uncertainty, it’s shaping up to be the stuff of financial nightmares.

In this post, we’ll unpack what Section 296 really means, who it affects, why it’s causing such a stir and what you can do about it.

What Is the New Division 296 Tax?

It’s important to note that this new tax won’t replace or change the current tax rules for super funds. For example, the standard 15% concessional tax rate on a fund’s taxable income will still apply, and eligible pension earnings will continue to be tax-free within the fund.

Instead, Division 296 is being introduced as an additional layer of tax—not a replacement.

This tax is designed to create a personal tax obligation for affected individuals. In other words, it’s not something your super fund will pay on your behalf—it’s a separate, individual tax bill.

Why is this Tax So Controversial?

The proposed tax will include tax on unrealised gains. This means if your superfund is $3 million and the assets in your fund go up in value, even though you have not sold them, they will pay tax on them. The issue is how superannuation funds will pay this tax if the funds assets are not liquid.

It's clear that this new tax is paving the way for a significant legal and political shift that could extend well beyond superannuation. If this proposal becomes law, what would prevent the government from targeting unrealised gains on your home, investment properties, shares, businesses, unpaid trust distributions, or private company accounts? In our view, this isn’t meaningful tax reform — it’s reckless economic policy.

Who Will It Affect?

Division 296 is aimed at individuals whose total superannuation balance (TSB) exceeds $3 million at the end of a financial year.

A few key things to know:

- This $3 million figure is set in legislation and won’t automatically increase over time (i.e., it’s not indexed).

- Even if your super is below $3 million, over time its likely that more people will be effected by this tax as their superfund balances grow.

-

It’s a personal threshold—not a combined one. So if you and your partner both have high balances, each of you is assessed separately.

- It doesn’t matter how many super funds you have—the total across all of them is what counts.

Who Has to Pay the Division 296 Tax?

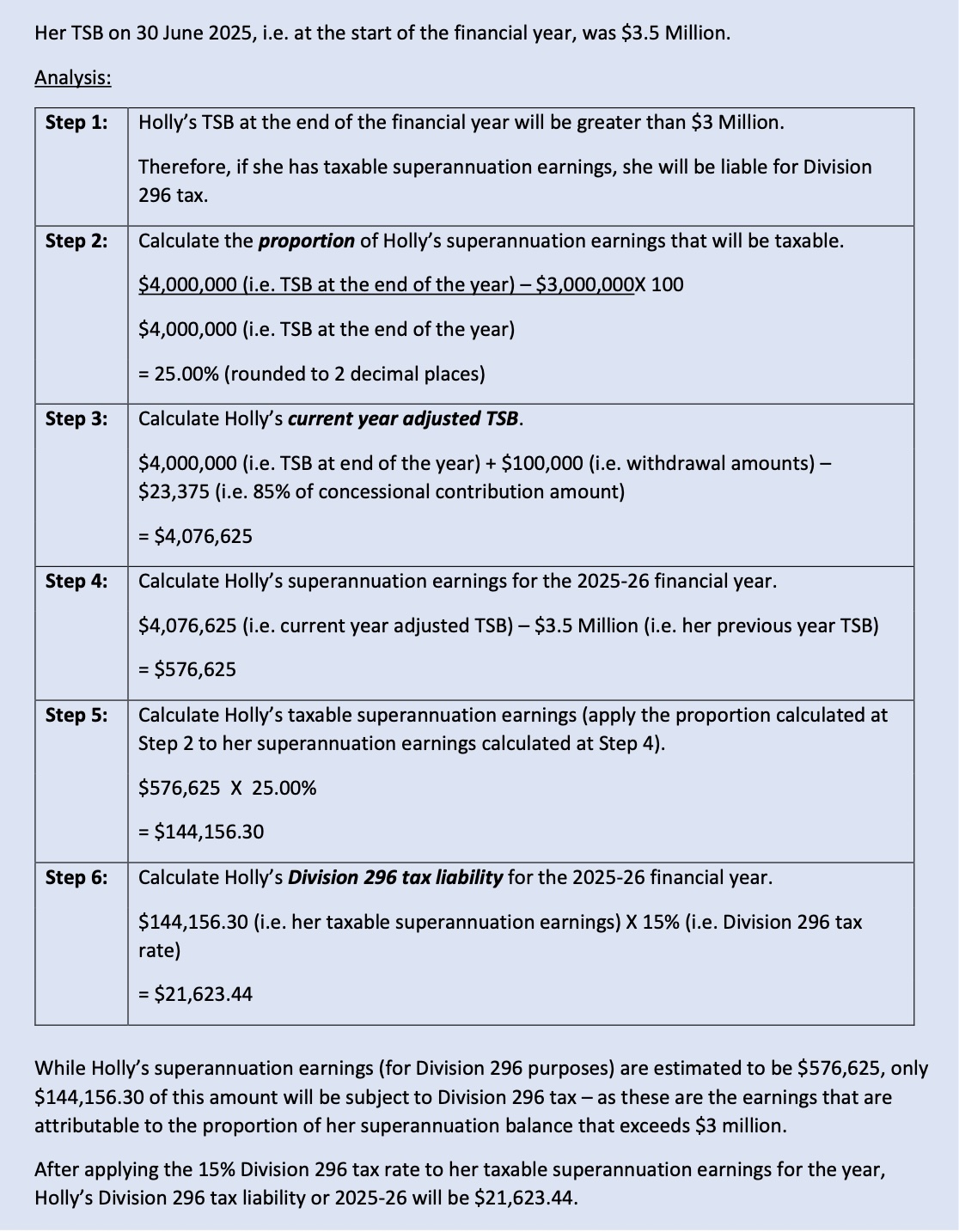

The first thing to figure out each year is whether someone actually needs to pay the Division 296 tax. That all comes down to their total superannuation balance (TSB) as at 30 June of the financial year in question.

If your TSB is more than $3 million at that point, and you’ve earned what’s called taxable superannuation earnings(we’ll get into what that means shortly), then you could be on the hook for this new tax.

In short:

- If your TSB is $3 million or less – no Division 296 tax.

-

If your TSB is over $3 million – you might owe the tax, depending on your earnings in the

fund.

What’s the Tax Rate Under Division 296?

If it turns out that someone does need to pay Division 296 tax, the amount they’ll be taxed is 15%—but only on a portion of their super earnings.

How is the Tax Calculated?

Step 1: Work out the portion of your fund that is subject to the tax

That 15% rate won’t apply to all of your superannuation earnings—just the part linked to the amount of your balance over $3 million. So, it’s a targeted tax, not a blanket one.

To work out what percentage of your earnings is affected, this formula will be used:

(Your total super balance at 30 June – $3 million) ÷ Your total super balance at 30 June × 100

For example: Let's say you had someone with a total super balance of $4 million at June 30. Then

the calculation would be: ($4m less $3m) ÷$4m x 100 = 25%.

This gives you the proportion of your earnings that will be subject to the 15% tax rate. Essentially, the more your balance exceeds $3 million, the bigger the slice of your earnings that gets taxed.

The formula used under Division 296 is specifically designed to make sure you’re only taxed on the part of your super earnings that relates to the portion of your balance over $3 million. So, if only a small part of your balance is over the cap, then only a small part of your earnings is affected.

Step 2: Work out what counts as superannuation earnings

Once it’s clear that you’re above the $3 million threshold, the next step is to figure out how much of your super earnings could actually be taxed under Division 296.

But this isn’t just a straight look at your super fund’s growth. Instead, your superannuation earnings (for Division 296 purposes) are calculated using a slightly adjusted version of your total super balance (TSB).

Here’s the general idea:

- Take your TSB at the end of the financial year.

- Add back any withdrawals you made during the year.

- Subtract any contributions (like employer or personal contributions) that went in during the year.

This gives you what’s called your adjusted TSB at the end of the year.

Then you compare this adjusted figure to your TSB at the start of the year. The difference between the two is treated as your superannuation earnings for Division 296 purposes.

This method is meant to reflect just the actual earnings (like investment returns) in your fund—not changes

caused by putting money in or taking money out.

Paying the Division 296 Tax

Similar to Division 293 tax, any Division 296 tax that’s owed is the responsibility of the individual – meaning, it’s up to the taxpayer to ensure the bill is paid.

When someone becomes liable for Division 296 tax, the ATO will usually send them a formal notice of assessment. Once this notice is issued, the tax must typically be paid within 84 days.

There are a few ways a taxpayer can pay their Division 296 liability. They can:

- Withdraw funds from one or more of their super accounts,

- Use personal or external funds, or

- Combine both options.

This choice is available even if they haven’t satisfied a condition of release under superannuation rules.

What You Can Do About It

With the upcoming changes to how larger super balances are taxed, many are wondering: Will this affect me, and if so, should I be making changes now? As with most tax matters, the answer depends on your personal situation.

If you're thinking about pulling out of super altogether because of the new tax, consider this: you’d need to weigh the new super tax rates against the tax rates you'd face in another investment structure. And don’t forget the transaction costs of moving assets around.

If your super includes long-term growth assets, now may be the time to review your portfolio and consider your options. Possible strategies include:

- Withdrawing assets from super if you have access

- Rebalancing across your family group, moving growth assets out of super and replacing them with income-focused assets

- Selling assets where it makes sense

- Leaving things as they are

- Or using a combination of these approaches

The right decision will depend on your personal financial goals, age, retirement timeline, and tax position.

As we mentioned earlier, the new Division 296 tax isn't law yet. Even if it does get passed, there’s a chance it could look different from the version we’ve described here. Right now, the Bill is being reviewed by a Senate Committee, and while there’s still a push to scrap or change it, it’s slowly moving forward. That’s why it’s a good idea to start getting familiar with how it’s currently expected to work, so you can be ready if it goes ahead.

Chris

Tolevsky is a Specialist Medical Accountant with over 30 years experience in the medical and allied health fields. He provides expert

guidance on tax strategies, building and protecting wealth . If you’re interested in discussing how we can help you please book

a complimentary consultation.

Chris

Tolevsky is a Specialist Medical Accountant with over 30 years experience in the medical and allied health fields. He provides expert

guidance on tax strategies, building and protecting wealth . If you’re interested in discussing how we can help you please book

a complimentary consultation.

Disclaimer: This article contains general information only . It is not designed to be a substitute for professional advice and does not take into account your individual circumstances, so please check with us before implementing this strategy to make sure it is suitable

Arrange Your FREE

No-Obligation Meeting

Please complete the form below

Download now and get your

business off to a flying start!