The Best Structure for Property Developers

If you’re a property developer, the way you set things up at the start really matters. Not just for tax, but for protecting your family and your future.

A good structure isn’t about being clever or complicated. It’s about making sure the risky part of property development sits in the right

place, and your personal assets stay out of harm’s way.

At the centre of this is one simple idea: separate the person taking the risk from the assets you want to protect.

Risk Taker vs Risk Averter

Most family-run development businesses naturally have two different roles, even if they’ve never thought about it this way.

There’s usually one person who is actively running the development. This person deals with the bank, negotiates with builders, signs contracts and gives guarantees. This is the risk taker, because if something goes wrong, they’re the first one exposed.

Then there’s usually another person whose role is to protect the long-term family position. They’re not involved in the day-to-day running of projects and they’re not signing guarantees. This person is the risk averter, and their job is to keep important assets, like the family home, out of reach of development risk.

Problems arise when these two roles are mixed together!

A Real-World Example

Let’s look at a typical developer couple, Tom and Sarah who want to do a property development and sell it after completion.

Tom is the one running the developments. He finds sites, speaks with builders and consultants, works with the bank and signs the contracts. Because of this, Tom is clearly the risk taker. In a sensible structure, Tom is the director of the development company and controls the decisions, but he doesn’t hold major personal assets in his own name.

Sarah, on the other hand, isn’t involved in running the projects. She’s focused on protecting the family’s long-term security. Because she’s not taking on development risk, it makes sense for Sarah to own the family home and stay outside the firing line if a project runs into trouble.

Note: If the family home is owned in joint names, you should consider having the husbands share transferred to the wife. This separation isn’t about one spouse having more control than the other. It’s about putting risk where it belongs.

How the Structure Works

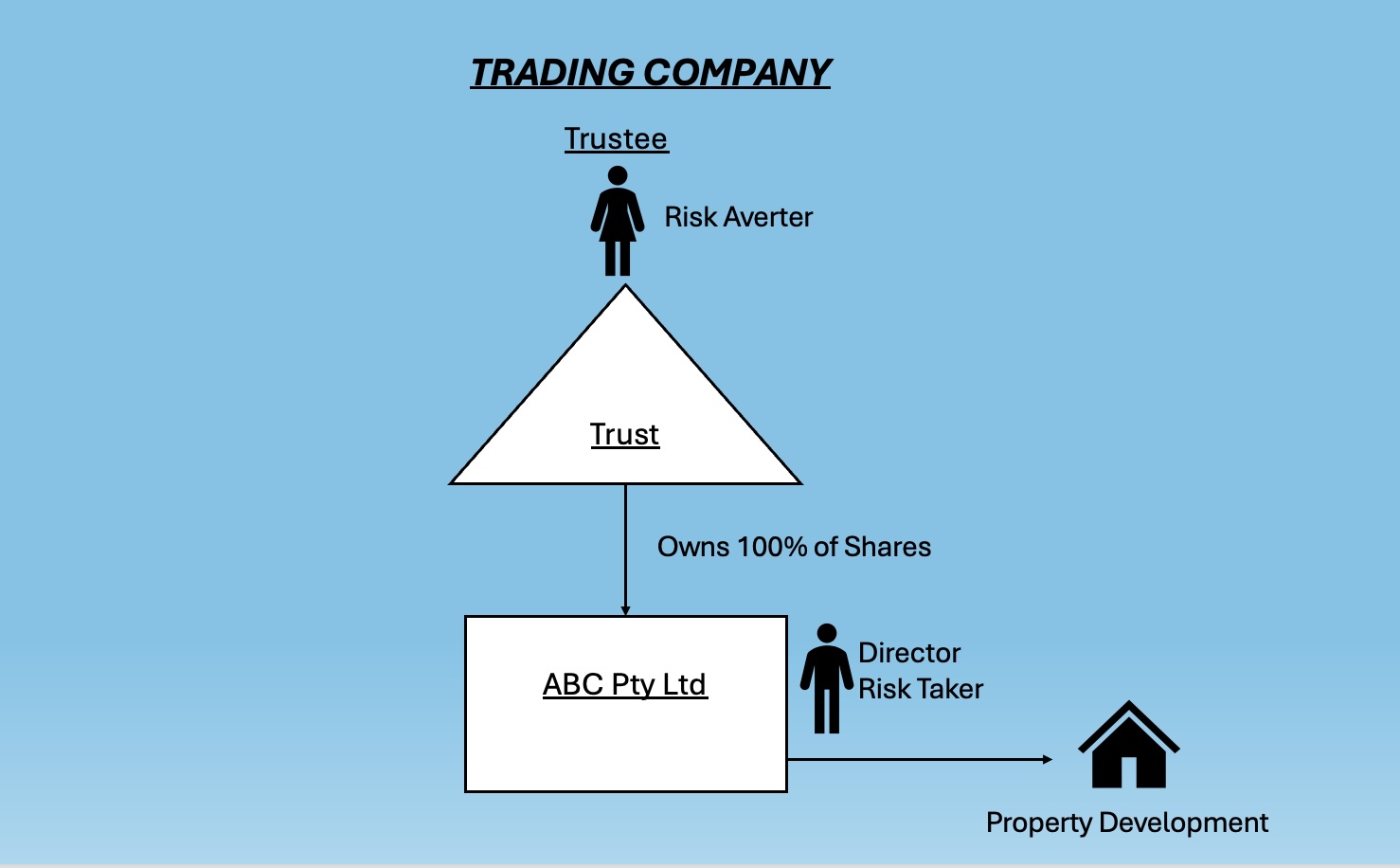

The structure that often works best for developers is a Company knows as doing the development work, with a discretionary trust owning 100% of the shares in that company.

The Company buys the site, builds the project and sells the finished properties. That’s where the risk sits. At the same time, Tom, as the risk taker, is the director the Company. He runs the projects, makes the decisions and deals with the banks and builders. He controls the business, but he doesn’t personally own the assets that need protecting. Sarah, as the risk averter, sits at the top as the trustee of the family trust.

It looks like this:

Note: For situations where you have multiple parties involved you would just have a Company and then each party would hold their

percentage share of the Company in a separate Trust.

What This Looks Like With Real Numbers

Let's say the Company completes a project and makes a profit of $400,000 after all expenses. The Company pays tax at 25%, which is $100,000, leaving $300,000 after tax. That $300,000 can then be paid to the Trust as a fully franked dividend.

The Trust can distribute this income to Tom and Sarah, who pay tax at their own marginal tax rates but receive a credit for the tax already paid by the Company. The Trust can also be distributed to other family members, helping to reduce the overall tax paid.

Alternatively, the Company can retain part or all of the profits. But beware, you cannot take the money out of the company without declaring a dividend because that would constitute a loan which would need to be paid back with interest and be put in place with a Division 7 a loan agreement.

Why This Structure Works So Well for Developers

For developers, this approach strikes a practical balance. The risky activity stays inside the company, personal assets like the family home are kept outside the danger zone, and profits can still be shared flexibly within the family. It also scales well.

You can use the same structure for multiple projects and add new project companies under the same trust as you grow. Most importantly, it recognises the reality that property development carries risk and plans for it properly.

The Key Takeaway

One of the biggest mistakes small developers make is putting the development, the risk and the family home all in the same place. That can work for a while, but when something goes wrong, the consequences can be serious.

A trust-owned Pty Ltd company, combined with a clear separation between the risk taker and the risk averter, is often a simple, effective

and protective way to structure a small development business.

The most important part is timing. This needs to be set up before you sign a contract. Once a project has

started, changing the structure is usually difficult and expensive.

If you get it right at the beginning, you’re not just planning for tax — you’re protecting your assets.

What If You Want Hold the Property as an Investment?

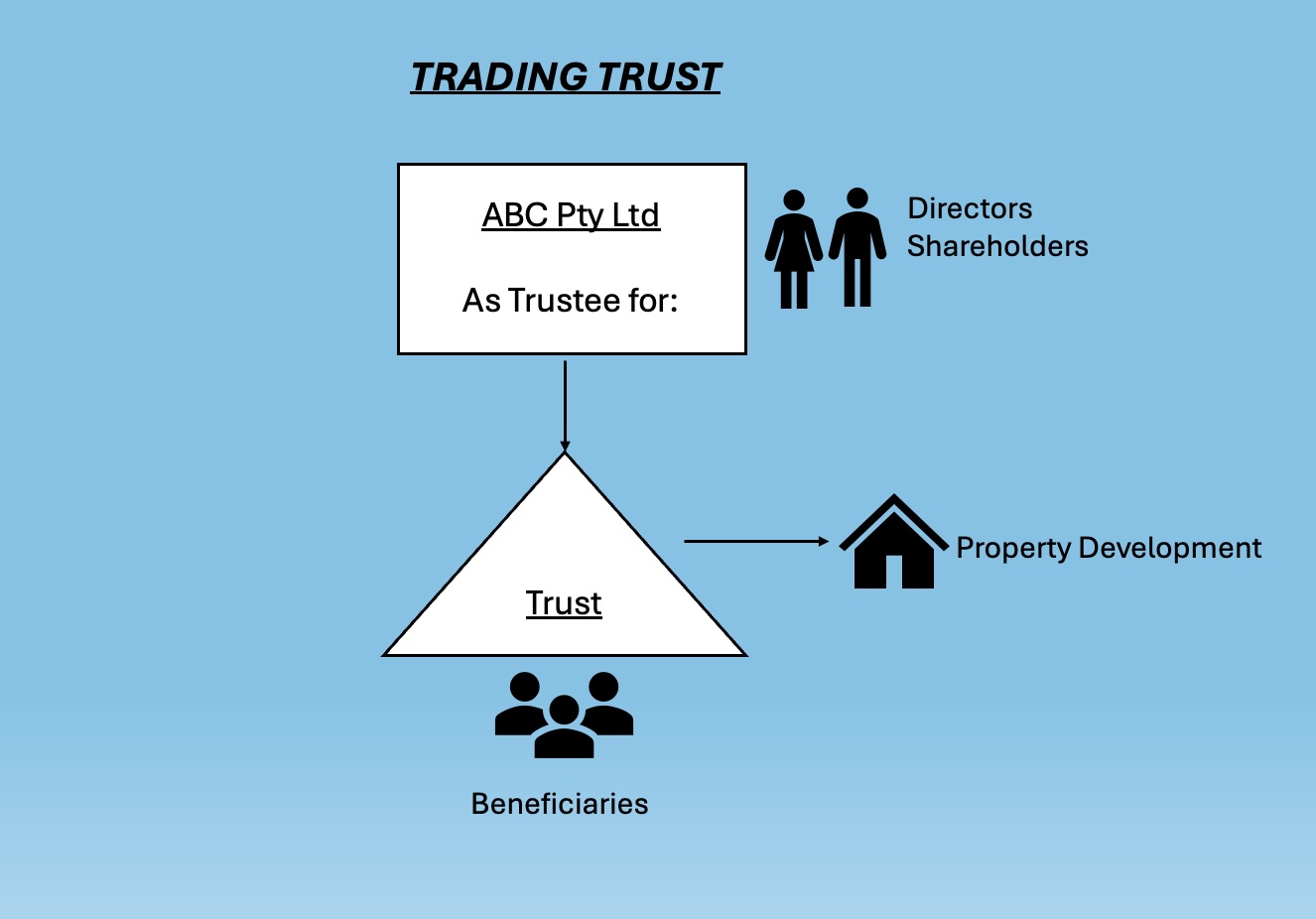

This is VERY important. If you do a development and decide to keep it for long term investment, we recommend that you set up a

different structure otherwise known as a Trading Trust with a Company as Trustee.

Under this structure, the Company acts as trustee for a trust, which is the entity that actually owns the property. The reason we use a

trust to hold the property is that, if a new residential investment property is held for more than five years — and is

genuinely rented out and not available for sale during that period — the trust will be entitled to the 50% capital gains tax discount when

the property is eventually sold.

It looks like this:

Note: For situations where you have multiple parties involved you would just have a Company as Trustee for a Unit Trust. Each party would then hold their share of Units in their own Trust.

The Bottom Line

Property development should always be treated like a business. Plan for taxes early, keep accurate records, and seek professional advice. Get your planning right, and you keep more of the profit you worked hard to earn.

We have over 30 years experience in dealing with property developers and can help you set up the right structure and put in place a simple book keeping system to keep track of everything, so that you can focus on what you do best. If you need help, please book in a complimentary consultation today.

Want to learn more?

Please click on the links below to view articles in our three part series on Property Development

Part 1: The Best Structure for Property Developers

Part 2: What Property Developers Need to Know About GST

Part 3: What Property Developers Need to Know about Finance

Arrange Your FREE

No-Obligation Meeting

Please complete the form below

Download now and get your

business off to a flying start!