Service Trusts Explained: A Practical Guide for Doctors & Dentists

Service trusts are a commonly used structure by doctors and dentists who operate private practices. When established correctly, a service trust can help separate practice operations, improve asset protection and provide a framework for managing practice expenses and business income in a tax-effective way.

First off, let's talk about the unfortunate truth doctors and dentists usually end up paying a hefty amount of tax. But don't despair, there are many ways to legally mimimise your tax. The problem is, there's a lot of misinformation out there. Many accountants, who are generalists and not specialists in this field, may give you incorrect advice. This could mean you're paying more in taxes than you should, or worse, you might get hit with penalties for using inappropriate tax strategies.

We are going to break down how taxes work for doctors and dentists , both in their employment and business income. We'll demystify income tax principles and explore the use of a Service Trust that could be game-changers for doctors and dentists.

Let's start by looking at the different scenarios in which doctors and dentists earn income and what the tax implications are:

Working as an Employee

Working as a Contractor

Now, most doctors and dentists in Australia work as contractors, which comes with some key differences compared to being an employee. As a contractor, you're often responsible for your expenses, and you might need to set up a company or trust to contract with the practice you are working from. However, this might not offer significant tax advantages. You'll need to register for an ABN and GST, and the practice will collect patient billings, deduct a management fee, and pay you the remainder. But here's the kicker – the practice won't withhold any tax, so you have to plan for your tax liabilities.

Unfortunately, being a contractor usually doesn't allow for income splitting with your spouse due to Personal Service Income (PSI) provisions. You'll need to include all billings in your tax return, claim deductions for management fees and other work-related expenses, and lodge a quarterly Business Activity Statement (BAS) to claim the GST credit. Your first tax return as a contractor will lead to quarterly income tax instalments, which can result in additional tax or refunds based on your income changes.

Running a Private Practice

Service Trusts

Doctors and Dentists often establish service entities for their private practices. These entities own equipment, employ staff, and cover business expenses. There are two main reasons for using a service entity: asset protection and tax planning.

Asset protection : Is vital because your service entity runs a business with inherent risks. Establishing the right structure can help separate those risks from your personal assets.

Tax planning : Comes into play because the income of your service entity is derived from dentists who use its services. These dentists typically pay a service fee, which can reduce your taxable income and divert income to the service entity. This entity should make a profit, which can be distributed to lower-taxed associates of the dentist, resulting in tax savings. e.g. The use of a "Bucket Company". It is important to understand that all distributions must be physically made beneficiaries including the "bucket company"

How does it work?

If you are a professional, e.g. accountant, lawyer, medical practitioner, dentist, or other professional and you could run your practice in a Trust structure, however as you are the one earning all of the income under your name, this income would be considered “Personal Services Income (PSI). This means regardless of the structure, you must receive 100% of the net profit.

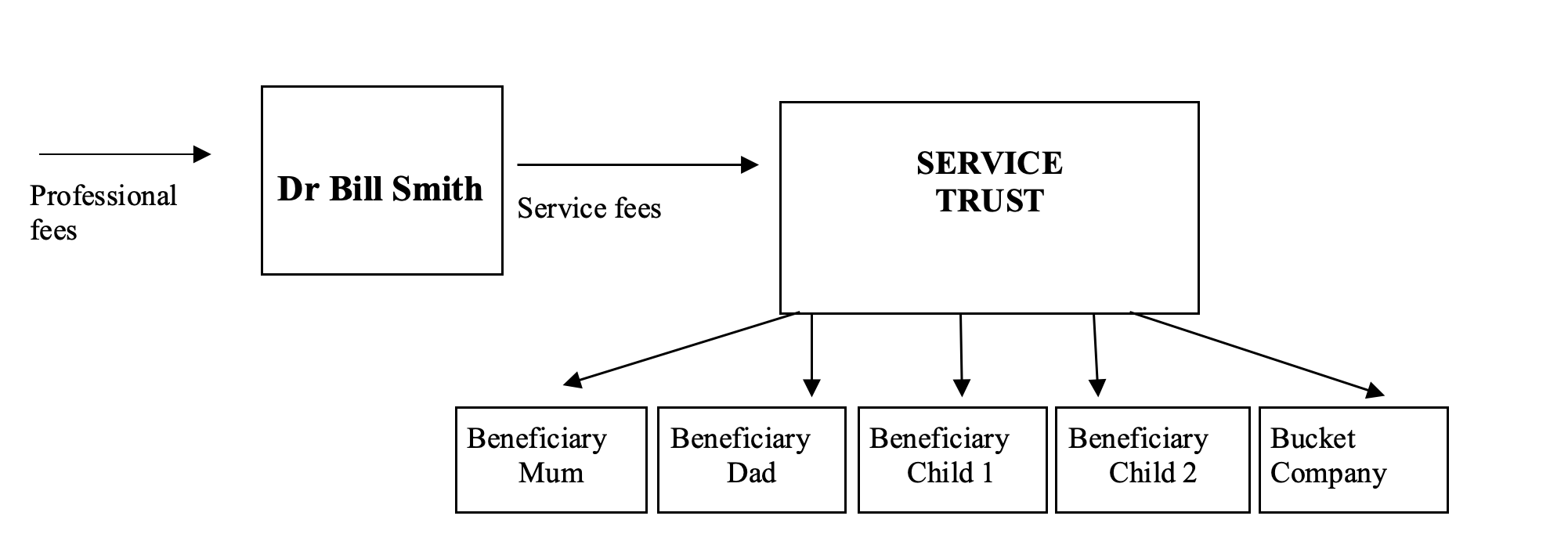

A typical structure for a professional would be to have the professional operate as a sole trader and then set up a Service Trust to run the practice and provide the professional with a place to practice from. This is just like a fully serviced office where you have a tennant and a landlord except the landlord being the Service Trust provides the premises and the administrative support for the professional.

For example: The doctor would earn all of his income from the medical clinic in his own name and bank this into his personal account. He would then pay for his personal business expenses such as service fees, car, medical subscriptions, professional indemnity cover, professional development etc. from this personal account. The doctor would then pay tax on his net profit.

The Service Trust would employ all staff and pay for all the running expenses of the practice, e.g. Rent, Utilities, Insurances, Equipment, In doing so, it would charge the doctor for these services by way of a mark- up. According to ATO guidelines, for GP’s, a service fee of 35% of gross practice fees would be considered commercial. For a dental practice, the service fee would be 60% of the dental practice’s gross fees. This relationship is documented in a Service Trust agreement betweeen the Professional and the Service Trust to ensure it meets the guildlines set out by the Australian tax Office.

The payment of a service fee will lead to profits being transferred into the service trust which can then distribute the income to the beneficiaries of the trust at a lower tax rate.

Case Example

Alternatively, If Bill sets up a service Trust, and all his practice running expenses are paid via his service Trust he could reduce his

tax. It works like this: Bill pays a service fee of 60% of his earnings to the service Trust, i.e. $600,000.

It looks like this:

The dentists Service Trust then pays the operating costs of the practice of

$ 350,000. This leaves Bill with a profit in his own name of $400,000 on which he pays tax of $149,592.

The service Trust will then have a net profit of $250,000, which he could distribute to the family members at lower tax rates and if required to a "bucket company" at a tax rate of only 25% or $62,500.

This results in an overall tax saving to Bills family of $55,000 per annum. It is important to understand that all distributions must be physically made beneficiaries including the "bucket company". Click here to read how bucket companies work

Need help?

Remember, it's crucial to consult with a specialist accountant to make the best financial decisions for your situation. At Tolevsky

Partners, we have specialised in working with dentists and other medical professionals for over 25 years, offering integrated tax ,

business and financial advice tailored to your needs. We are able to set up this complete structure, including all legal

agreements and make it easy for you. If you would like to discuss your personal situation please book here for a

complimentary meeting.

Arrange Your FREE

No-Obligation Meeting

Please complete the form below

Download now and get your

business off to a flying start!