From 1 July 2027, the Government is tightening the rules on negative gearing for residential property — but only for properties bought after 7:30pm on 12 May 2026, and mainly for established properties.

New builds are treated differently (we’ll get to that). So what does this actually mean?

First ,what is negative gearing?

Negative gearing is just a fancy way of saying...

You lose money on a rental property each year because rent coming in is less than costs going out (interest, repairs, depreciation, etc.). And under the old rules, that loss could usually be used to reduce your tax on other income — like your salary. That’s been one of the big drivers of property investing in Australia for decades.

The big change

Under the new rules, that flexibility gets tightened.

If you buy an established residential property after the cutoff date, you can no longer freely offset those rental losses against your wage or other income.

Instead, losses from established property can only be used against other residential property income, including rental income and capital gains from other properties

What happens to leftover losses?

If you can’t use all your losses in a given year, they don’t disappear.

They get carried forward.

And later, you can use them to offset future rental income, or capital gains when you eventually sell a property. So it becomes more of a timing issue than a total loss in many cases. But — and this is important — timing matters a lot here.

Because if you never generate enough future gains or income to use those losses, some of the benefit can effectively be delayed indefinitely.

Who gets caught by the rules (and who doesn’t)

The changes apply to:

- individuals

- companies

- partnerships

- most trusts

But there are important exemptions:

- superannuation funds (including SMSFs) are not affected,

- widely held trusts (like managed funds) are excluded

- some government housing programs and build-to-rent projects get special treatment

So it’s not a blanket rule across the entire system.

The “grandfathering” rule (this is important)

If you already own an investment property before the announcement date, you’re generally protected.

That means with existing properties stay under the old rules you can continue negative gearing them as before. Even if the property was bought under contract before budget night but not yet settled at the time, it’s still protected.

However, there’s a bit of grey area if a former home is later turned into an investment — and that detail may depend on how the final rules land.

New builds get special treatment

Here’s the carve-out.

If you invest in a new build, you can still access negative gearing.

And you may also get a choice when you eventually sell ,either the current 50% CGT discount, or the new indexation + minimum tax system. So the Government is clearly trying to keep incentives flowing toward new housing supply.

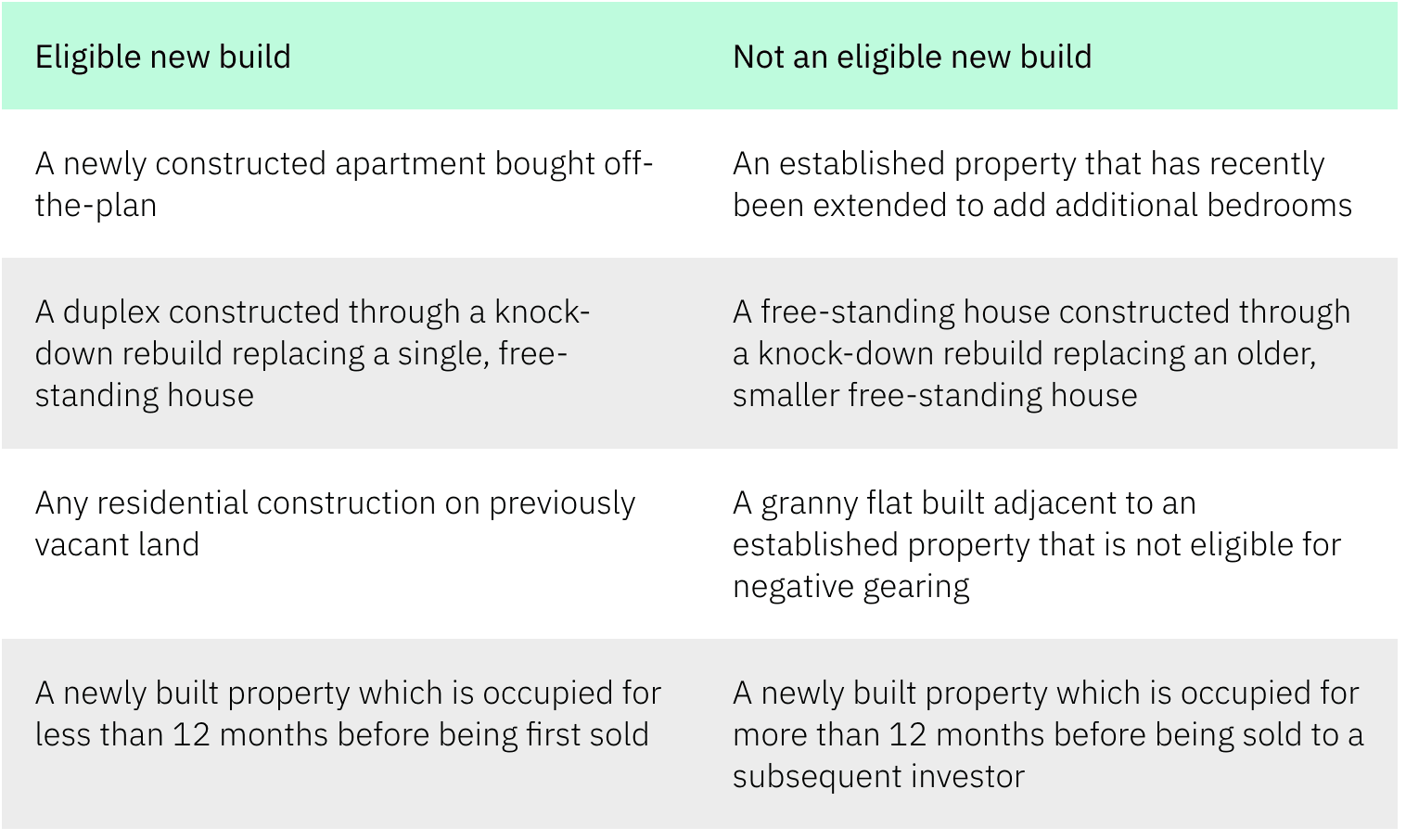

Here's a summary of what the government defines as a 'new build'

The big picture (what this really means)

If you step back, the direction is pretty clear: Negative gearing on established property is being limited.

Not removed completely — but tightened so that losses stay within the property system and can’t be freely used against other income anymore

At the same time new builds are encouraged, existing investors are mostly protected and losses become more about timing than immediate tax relief

The bottom line

For years, the strategy has been “Lose money on property, reduce tax elsewhere, and wait for capital growth.” That second part — reducing tax elsewhere — is what’s changing.

The system is shifting toward something more contained, where property outcomes mostly stay within the property world. And as always with tax changes like this, the real impact won’t just be in the rules themselves…

It’ll be in how investors need to rethink the way they structure, hold, and time their investments going forward.

Why negative gearing has never been the heart of my personal investing strategy ...you might be surprised!

I’ve never looked at property investing as a way to chase write-offs. To me, that’s putting the cart before the horse. An investment should stack up because it’s a good investment:

- quality asset

- long-term growth potential

- improving cash flow over time

- and the ability to build wealth steadily through compounding

If there are tax benefits along the way, great. But they’ve never been the reason I buy. Because at the end of the day, a deduction usually means one thing: you spent a dollar to get part of it back later. That’s not a strategy. That’s just easing the pain. So when governments start tightening negative gearing rules, I don’t see it as the end of the world.

Why?

Because my approach was never dependent on generating losses to make the numbers work. The focus has always been on owning assets that make sense financially first — with or without the tax perks.

And that mindset brings something pretty valuable in times like this: Stability.

For more information please visit our 2026 Federal Budget Hub

Part 1: Negative Gearing Changes

Part 2: Capital Gains Tax Changes

Part 3: Discretionary trusts minimum 30% tax

Arrange Your FREE

No-Obligation Meeting

Please complete the form below

Download now and get your

business off to a flying start!