How To Improve Your Cashflow #4

Many business operators base their prices on the competition. in doing so they assume the competition have their pricing structure right, that they are making a profit and that they have the same cost structure as themselves. In reality every business has a different cost structure and it is important to understand yours.

Some businesses reduce their prices to obtain a greater share of the market with the aim to increase their price later and hopefully end up with more market share than when they started. Unfortunately many who use this approach find out that volume is bought more easily than profits. There aren’t many wins with price wars. Those who last the distance are the ones with the least debt, the strongest balance sheet and know their costs.

By understanding your own cost structure you are able to answer questions such as: How many extra sales you have to generate to compensate for a reduction in your price? If you increase your price, you could assume that you may experience a decrease in sales. By how much can your sales reduce before it starts to affect your bottom line? How many sales do I have to make to cover my costs or just break even, ie: the point of no profit but also no loss?

Break even analysis is a financial tool that allows you to work these things out. This sounds like rocket science but in reality it is quite simple. Expenses in your business can be divided into two main categories. The first of these are fixed costs. These are those expenses not directly related to sales ie. they remain relatively constant regardless of the sales volume and includes rent, wages, rates and utilities.

All other expenses are known as variable costs and are directly related to the volume of sales, which means for every dollar you make you incur an additional cost eg. stock, materials, direct labour and commissions.

Often it is assumed that every dollar that comes into the business is another dollar to spend on something else. Unfortunately this is not the case. If your rent goes up by $10,000.00 the extra sales required to cover this cost will almost certainly not be $10,000.00 but will be dependant on your cost structure.

For example, let’s assume I sell pens. These pens cost me sixty cents to produce and I sell them for one dollar. Therefore, out of every dollar earned a portion of this is already spent. In this example the variable costs are sixty cents, which leaves me with forty cents in every dollar to contribute towards all other fixed costs. This portion of the dollar is called the contribution margin.

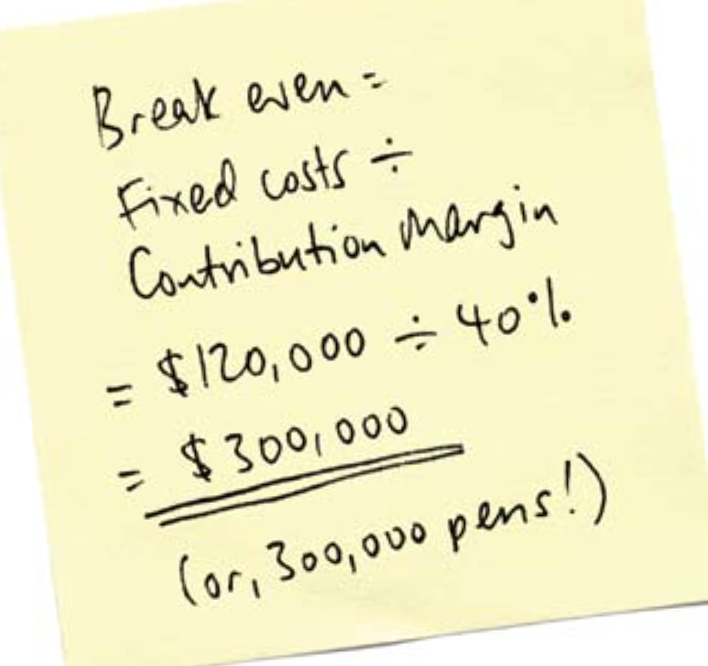

If the total fixed costs in my business add up to $120,000.00, how many sales do I have to make to break even? If we know that out of

every dollar earned we only have forty cents (or 40%) left to pay for our fixed costs and that our fixed costs add up to $120,000.00

then we can work out the sales required to break even.

If the total fixed costs in my business add up to $120,000.00, how many sales do I have to make to break even? If we know that out of

every dollar earned we only have forty cents (or 40%) left to pay for our fixed costs and that our fixed costs add up to $120,000.00

then we can work out the sales required to break even.

This is how many sales are required to break even, the point of no profit and no loss. To break even, you would have to make $300,000 in sales. i.e. $120,000 / .40 = $300,000.

If the business sold 301,000 pens they have only made a profit of forty cents, because out of every dollar sixty cents has to be spent to produce that pen.

Break even analysis is a powerful financial tool which can be used to measure the impact of a change in price, volume or costs and helps you plan and develop strategies to reduce the effect of these changes. If you are planning to buy a piece of equipment, take on a new employee, pay someone a bonus or want to set yourself a certain profit, break even analysis can be used to show you how many extra sales or additional production is required to cover these costs.

If you would like our help in improving your cashflow please arrange a chat with one of our expert team members.

Want to learn more?

Please click on the links below to view our 4 part series on "How To Improve Your Cashflow"

How To Improve Your Cashflow #1

How To Improve Your Cashflow #2

How To Improve Your Cashflow #3

How To Improve Your Cashflow #4

Arrange Your FREE

No-Obligation Meeting

Please complete the form below

Download now and get your

business off to a flying start!